In This Article:

- How to Turn a Thousand into a Million

- What’s a DRIP?

- What is the history of DRIPs?

- Compound Interest: The Most Powerful Wealth Building Secret Known to Man

What did one penny say to the other penny?

“Let’s get together and make some cents.”

I’ll see myself out.

Now, I’m a dad, and can get away with a “Dad Joke” here and there. But honestly, when it comes to making money, you can’t worry too much about being witty or fashionable.

Some strategies stand the test of time and can easily turn those pennies into dollars without you having to lift a finger.

In order to retire rich, you don’t have to day trade. You don’t have to buy options. You don’t have to speculate on sink-or-swim penny stocks. You just have to be patient.

As other elders have probably told you, the best time to start investing is yesterday. The next best time is today.

Let’s take a quick example from the realm of “what we should have done.”

I know from experience…

- My grandmother bought me savings bonds each year for my birthday and kept them in a special file. Once they matured, she gave them to me to help me buy my first car.

- My grandfather gave me gold and silver coins every year for Christmas — which are now worth far more than when I got them.

- My father regularly bought me stock in several companies, and when I turned 21, he handed them over to me. I thankfully still own most of them today…

So when my son turned four, I gave him the single most boring gift in the world: a stock certificate.

Now, I didn’t buy my son’s stock the “normal way.” I started him on a stock plan called a “Dividend Reinvestment Plan” or a DRIP.

What is a DRIP?

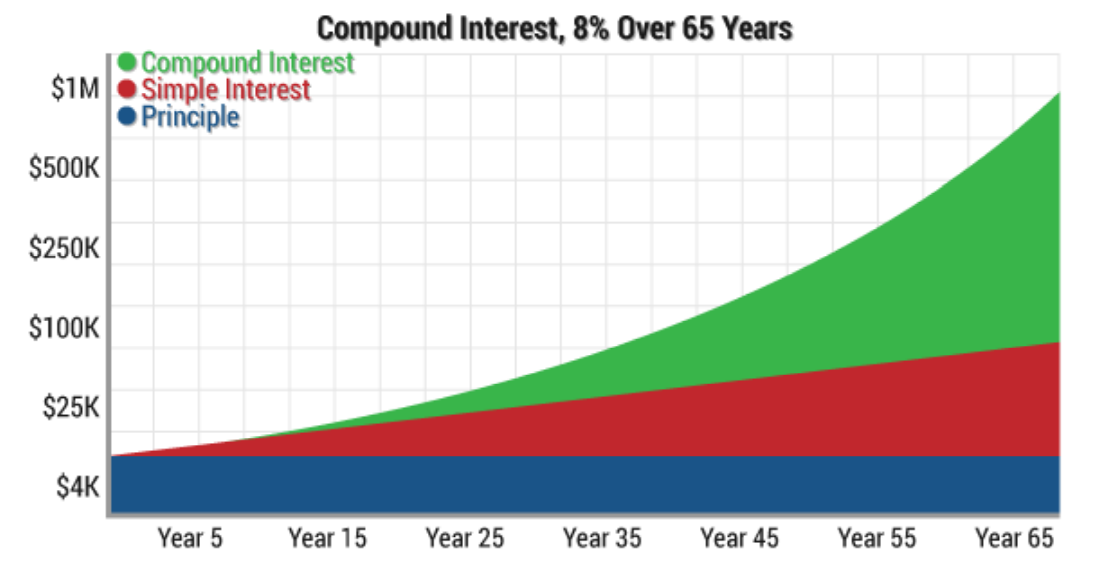

If you invest $4,000 into a DRIP around the birth of a child or grandchild and let it ride — meaning you never even contribute another penny to that investment — that $4,000 will compound to around $1 million by the time they turn 65.

DRIPs allow your dividends to compound like they’re on steroids. So if you want your little one to retire a millionaire, it is rather simple, as long as you start a DRIP plan early.

Just take a look at this chart:

That is assuming a 8% return — which, with most of the plans I’ll recommend, is completely within the realm of possibility.

If you make semi-regular contributions — say as part of their birthday present each year — that number will be far higher.

But the earlier you start, the better.

What is the History of DRIP Stocks?

DRIPs began as a company stock program that was — at the time — only available to employees of a select group of companies. It allowed company workers to purchase shares of their employer — often at a discount.

This was a big success for companies, considering they could create a long-term and stable core of shareholders who conveniently are incentivized to work harder and boost productivity. It was a win-win situation. But there was the issue of what to do with the dividends the companies owed to the employees. The company would have to do a lot of work to calculate the dividends and provide a dividend payment. In the end, a lot of the workers just ended up putting the money back into the company’s stock.

Employees were given the opportunity to just reinvest their dividends into more shares or fractions of shares. Now there was no need to shuffle money all over, the company could count on continued purchases of shares by long-term stable investors, and everyone was happy.

Employees enrolled in DRIPs never had to check their portfolio, never paid trading fees, and didn’t have to fork over 3% of their wealth for a money manager to move around a basket of stocks. Their investment was locked in on autopilot, and they made more and more money every year without anyone having to lift a finger.

Compound Interest: The Most Powerful Wealth Building Secret Known to Man

Compound interest is perhaps the most powerful wealth-building secret known to man. It’s quite simple: your interest payments buy more shares, which raises your stake in the company, and then the interest payments keep growing as you accumulate more shares.

It is a set-it-and-forget-it strategy that will allow you to compound the interest on your stocks without having to do practically anything.

You can think of it as “interest on interest,” and it will make an investment grow at a much faster rate than simple interest. Many of the greatest minds in history knew this and profited from it.

Take founding father, Ben Franklin, for example. He was well known for platitudes like “a penny saved is a penny earned,” “an investment in knowledge always pays the best interest,” and “I’d rather go to bed without dinner than to rise in debt.”

But he didn’t just talk — he put his money where his mouth was.

Way back in 1785, French mathematician Charles-Joseph Mathon de la Cour ridiculed Franklin’s book Poor Richard’s Almanack as being “too optimistic.” He wrote a scathing critique about leaving a small amount of money in a will only to be used after it had collected interest for 500 years.

Little did he know that Ben was listening…

Franklin wrote to Mathon de la Cour and thanked him for such a great idea, telling him that he had decided to leave a bequest to his native Boston and his adopted Philadelphia of 1,000 pounds sterling to each city, with the condition that it was put into a fund that would gather interest over a period of 200 years. That small stake in Philadelphia turned into $2,256,952.05 since Franklin died in 1790.

The bulk of Franklin’s investment will be used to assist recent graduates of Philadelphia high schools in pursuing careers in trades, crafts, and applied sciences. Franklin’s Boston trust fund, however, is worth almost $5 million. Now, Ben Franklin wasn’t the only genius that got behind this idea…