Public WARNING Issued on Behalf of Millions of Americans…

2023:

Congress Comes for Your Retirement Money

New Law Set to Devastate Your 401(k)s, IRAs & Roth IRAs…

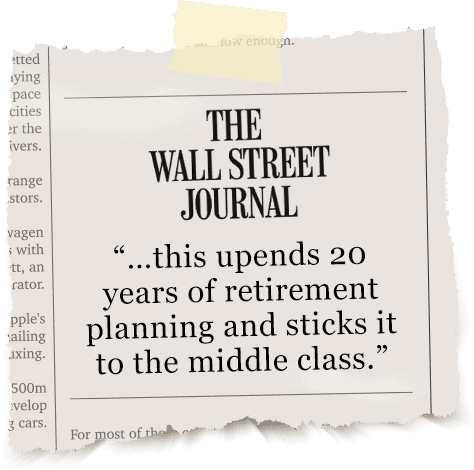

“Upends 20 Years of Retirement Planning and STICKS It to the Middle Class.” —The Wall Street Journal

Hi, Bob Carlson here… founder of The Center for Retirement Security.

I’m speaking to you today because the U.S. government just enacted the most devastating law I’ve seen in my 30-plus years as a retirement expert.

This new law is set to significantly reduce the value of your 401(k)s… your IRAs… (yes, even your Roth IRAs)… and even your pension, if you have one of those.

Everything you’ve worked for… All that money you’ve put away… And the years you spent saving.

This Congress is taking it away.

Trust me, American retirees are about to suffer a serious blow.

But don’t just take it from me.

Look at what The Wall Street Journal reported, and I quote: “…this new law upends 20 years of retirement planning and sticks it to the middle class.”

The online media outlet Salon confirmed this: “If you thought it was a safe bet to put your money into retirement plans over the span of your career for estate planning, think again.”

Look, this hits me personally. And it will hit just about anyone with money put away in a retirement plan.

And that’s not the worst of it.

David Phillips is a noted estate planner and bestselling author, and he calls it: “the biggest tax to hit your estate since 1913.”

Listen, this new law is set in stone…

Which obviously gives you very little time to actually do something about it.

It’s no wonder the people I work with are scrambling to save their retirements.

They don’t want to see everything they’ve worked for taken away.

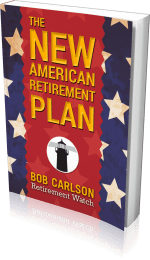

That’s why I’ve spent the past 12 months putting together a new book… and I’m going to give you a copy of it at the end of this brief presentation.

It’s called the NEW AMERICAN RETIREMENT PLAN.

Think of it as your Retirement Survival Guide for keeping the government’s new rules at bay.

Following its steps won’t just be your best defense against this damning new law…

It could literally SAVE YOUR RETIREMENT — a hundred times over.

As I said, I’m going to send you a copy completely free of charge today.

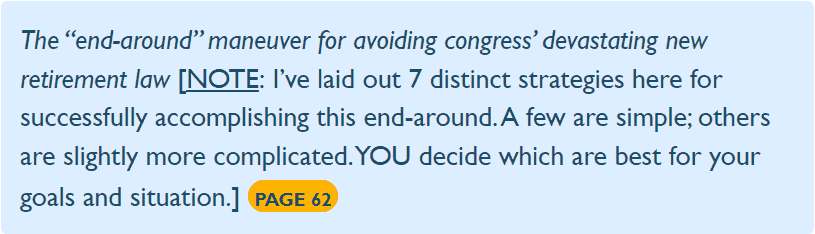

In fact, on PAGE 62, I’ll tell you the very first move you need to make to save your IRAs and 401(k).

(It’s the first of seven “end-around maneuvers” you can use to stop the government in its tracks when it comes for your retirement money.)

And that’s just for starters.

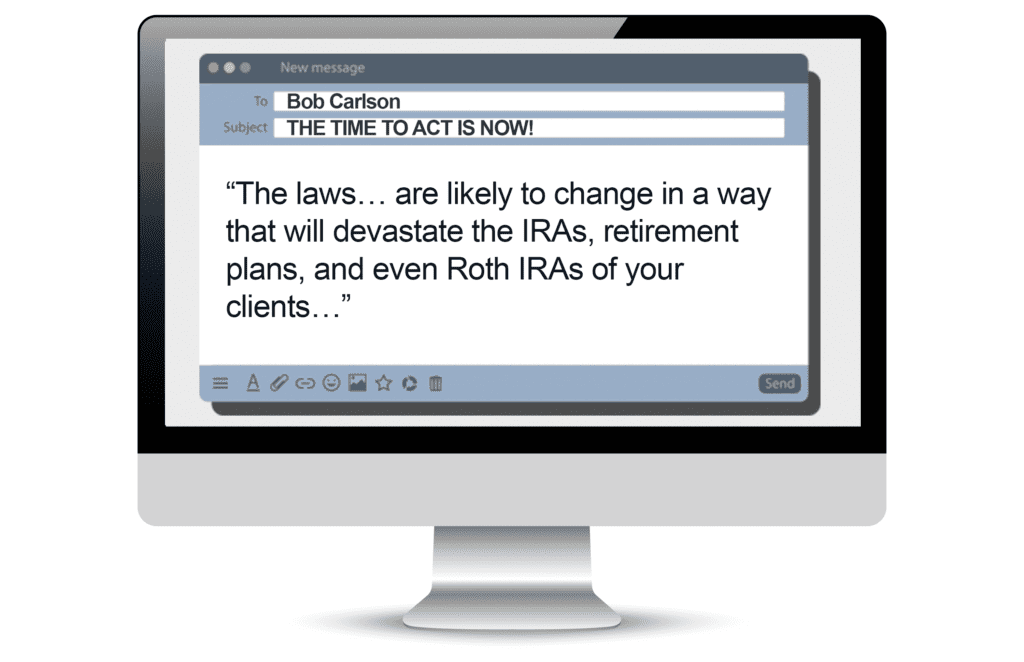

Here’s an email from a retirement insider contact of mine – which says it all.

The subject line of his note reads, “… THE TIME TO ACT IS NOW!”

He goes on to say, “The laws… are likely to change in a way that will devastate the IRAs, retirement plans, and even Roth IRAs of your clients…”

Look, it’s downright scary to think what the government has in store for your retirement funds.

And it’s high time the truth came out…

Because we’re now at a crisis point for every American who’s retired or planning their retirement.

And I’m not going to mince words. Retirement Doomsday is coming — whether you’re ready for it or not.

I’m warning you now, because I don’t want a single person left behind when it hits hardest — and starts tearing apart your 401(k)s, IRAs and Roth IRAs.

So if you want to save your retirement account — and keep the IRS from confiscating 30% or more of it…

I urge you to pay close attention.

April 2023:

Your Retirement Plan is about to Get Whipsawed

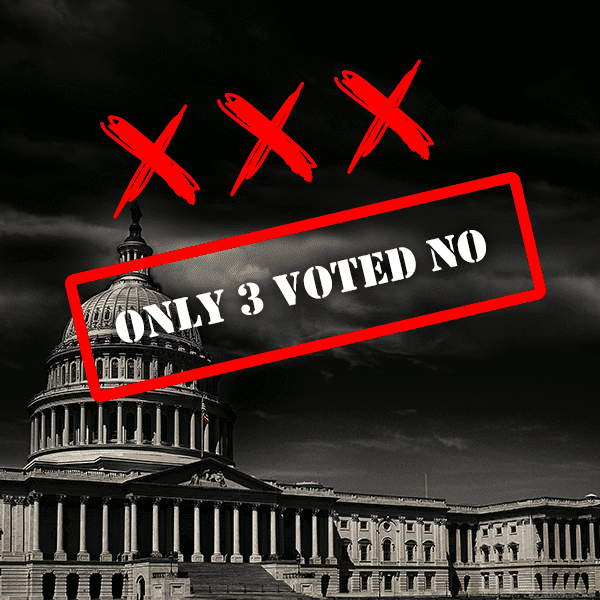

Most people have no idea this legislation just fast-tracked its way through Congress.

With everything happening in the world right now, it’s getting even less coverage than it would in normal times.

The House passed it by an overwhelming margin. Only 3 of 420 elected representatives voted NO… and 15 reps didn’t even bother to show up.

The bill stalled for a while, before breezing through the Senate, then getting signed into law by the president.

The whole thing happened very quickly…

Just 1,500 feet away from my 5th floor office at The Center for Retirement Security.

And now… the retirements of so many Americans… are about to go up in smoke.

As the local DC Report just published in a scathing piece:

“Congress Targets Middle-Class Retirement Savings.”

Yet, virtually nobody outside Washington in mainstream America saw this coming.

So let me paint you a picture of what this all means.

Let’s say you’re a 62-year-old who has socked money away all your life.

You’ve done so to ensure a comfortable retirement, on your own terms.

What’s more, you want to extend your retirement savings to your loved ones after you pass on.

That includes your 401(k)s… traditional IRAs… even your Roth IRAs.

Naturally you want your hard-earned (and growing) money to last as long as it can, and — just the same — to get taxed as little as possible.

Brace yourself. Because the rules we’ve grown accustomed to are getting completely upended by Congress.

I’m talking about the same laws that have helped make the growth of our nest eggs possible!

Put plainly, Congress is changing the retirement rules, in a severe way. This time won’t be the last, either.

And too many retirement-age Americans are going to suffer for it.

As The Wall Street Journal reported, “…Congress can’t wait to get its hands on America’s retirement-account assets.”

In short, what the government wants to do is strip the value of your IRA or 401(k) before you can pass it along to your family.

Yet, the shocking thing is, they think of this as a good thing!

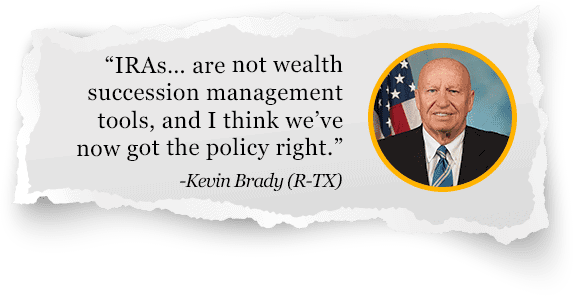

One U.S. Congressman — Kevin Brady (R-TX) — put it quite bluntly…

And that’s just from one side of the aisle.

Also in the House, there’s Majority Leader Steny Hoyer (D-MD), who said…

Of course, considering today’s polarized and dysfunctional Congress, you may be wondering:

How did this law even get passed?

Valid point. But here’s the thing:

These bloodsuckers just want more money.

That’s the cold, hard truth. And they’ll do anything to get it.

Which is why I’m sounding the alarm… to let as many people know that the TIME IS NOW to revamp your retirement plans.

You simply cannot risk your life savings by not acting.

When this new law really kicks in, you’ll come to know this as fact…

Uncle Sam Is After Your Retirement Money

And it doesn’t even matter how much or how little you have.

If your money’s in a 401(k)… they’re coming for it.

If it’s in a traditional IRA or a Roth IRA… they’re coming for it.

Heck, if it’s in your kids’ or grandchildren’s college funds… they’ll come for that, too.

The Wall Street Journal summed it up like this: “…a college planning nightmare for middle-income parents.”

As I said, they’re hot on the trail. Only this time, it’s not just your money they’re after.

It’s also your heirs’ money that’ll get looted.

In other words, your legacy is under attack.

And that’s just the first in a series of nefarious plots they’re planning.

Truth is, the government needs to raid our retirement funds now more than ever.

Of course, Congress never passes a bill that’s painful for citizens…

Without making it seem like a benefit.

They want you to read the headline. But not the substance.

In this case, they’re working to expand every American’s access to retirement plans… along with making these plans more flexible and less expensive.

Seems nice, and rather generous, right?

Sure. Until you get to the dark underbelly.

The part that undermines and undercuts your hard-earned savings.

The part that puts an end to the rules that have actually helped us all this time.

That means you have precious little time to protect your 401(k)… your IRAs… and your Roth IRAs from Uncle Sam’s “2020 heist.”

You want to act right now…

Before they get the green light to ravage your retirement.

Before your family gets hit with massive and accelerated income taxes.

Fortunately, I’ve identified a handful of solutions.

And the best place to start, I’ve found, is knowing how we got here in the first place.

They Set “The Trap” Decades Ago. Millions Are About to Get Caught in it.

In the 1970s, retirement savers were handed the gift of a lifetime when traditional IRAs became available to the public.

Back then, the maximum contribution was only about $1,500.

Over time, the maximum contribution increased, as did the number of Americans who participated.

A few years later in 1978, the 401(k) was established.

American workers fell in love with this plan.

And the love keeps spreading — with as much as $5.8 trillion currently wrapped up in 401(k) assets.

And by the time the Roth IRA became law in 1997, retirement savers acquired yet another way to prepare for their golden years.

Armed with these new savings strategies, retirees now had what no one could’ve predicted…

Three unique, tax-advantaged, wealth-building strategies.

A blessing, to be sure.

Until, of course, it’s not…

And that day has arrived.

You see, America has roughly 75 million baby boomers.

That’s almost one quarter of the country’s population.

Many of whom — over the past few decades — have contributed as much of their paychecks as possible into their Roth IRAs, traditional IRAs, and 401(k)s…

That’s literally trillions of dollars tied up in these retirement vehicles.

Yes, trillions.

And those baby boomers — maybe you’re one of them — are starting to retire.

More and more each year, in fact.

And all those nest eggs?

They’re getting cracked open.

To pay for retirement expenses. College tuition. Weddings. You name it.

So think for a second how you’d feel…

Needing immediate access to your nest egg — but suddenly discovering…

Congress Just “Raised the Toll” to Tap Your Retirement Accounts

(You’re Paying MORE to Get Your Money)

Get ready for the new normal.

It’s going to cost you more to tap into your retirement funds.

Talk about getting fleeced!

You see, Congress has no choice.

Not with how much debt they’ve run up over the years.

Not when faced with Social Security’s trust fund running out in 2034.

And certainly not with Medicare getting more expensive each year, as baby boomers get older.

No, Congress’ plans — however fiendish and diabolical — are simple.

If they want to pay the bills…

They have to come for your money — a “cash grab” of the highest order.

In other words, Congress giveth.

And, now, Congress taketh away.

For decades, they gave us all kinds of tax incentives to put as much money as we could into retirement accounts.

Today they’re putting the screws to us… by increasing the tax charges for taking that money out.

And it doesn’t end there.

We’ve just seen the first of a series of actions by Congress and the I.R.S.

All specifically designed and directed to increase taxes on all retirement accounts and IRAs.

It could even prevent you from qualifying for financial aid for your college-bound kids. (I explain how on page 187 in the NEW AMERICAN RETIREMENT PLAN.)

Plus, there’s evidence pointing to one of retirees’ biggest fears coming true…

That future Roth IRA distributions won’t be what they were intended to be all along: Tax-Free.

I don’t know about you, but it all scares the living heck out of me.

And what I’ve just described isn’t even the most urgent news!

As I said earlier…

The bill that steamrolled through Congress has now taken effect — with a mandate so crippling…

America’s retirement dam will effectively burst.

And the aftermath? Catastrophic.

People who’ve worked most of their lives…

Played by the “rules”…

Saved for college, and saved for their retirements…

Are about to face a day of reckoning.

Millions of Americans will see an extra tens of thousands… hundreds of thousands… even millions of dollars — taxed away.

The great retirement blood-letting has begun — and it gets even worse in the coming years.

So not only are you being screwed NOW…

The same will be true for your heirs and their future generations.

Mark my words. This is just the beginning, folks.

It’s hatchet job number one in a string of similar actions Congress has planned — to seize more and more of your retirement nest egg.

I’ve seen this coming for a while now. That’s why I’ve spent the better part of 12 months putting together the NEW AMERICAN RETIREMENT PLAN…

To protect as many of my family members, friends, readers, business associates — and regular investors — from the devastation that’s coming.

In my new book, I detail exactly how to keep the IRS OUT of your retirement accounts.

I’ll show you how to protect your money… but ALSO how to grow your money substantially.

And in a minute, I’ll show you how to get a free copy.

But first, you’re probably wondering…

Why Haven’t I Heard About This Retirement Doomsday Event In the News?

For starters, the “news” is hardly news anymore.

To get the truth, you can’t pay attention to all the agenda-driven talking heads poisoning TV’s airwaves.

You have to search it out for yourself. It won’t be handed to you on a silver platter.

And I really don’t care which side of the fence you sit on, politically speaking.

That’s not why I’m sounding the alarm today.

My message is clear and free of bias. And it boils down to this:

If you’re at all concerned about your retirement finances, you’ll put the “noise” you hear in the news to the side.

And you’ll make sure you have all the facts — BEFORE this Retirement Attack takes hold over the next few months.

I’m talking about the same facts, and the exact series of steps I’m personally using to protect my own family.

Bottom line: I’m going to rush you a copy of my new book, the NEW AMERICAN RETIREMENT PLAN.

I won’t charge you for it.

I’m doing this because I’m convinced the strategies laid out in its pages will help Americans save their retirement finances in a multitude of ways.

Now I’m not the only retirement expert pounding his fist right now.

David Phillips is a highly regarded estate planner with 42 years’ experience. He’s also a trusted friend.

Like me, David kept close tabs on every formal and nuanced step of this legislation.

And when he confided that this congressional money grab could be the biggest tax hit to Americans’ retirement plans in over a century…

Sadly, I couldn’t agree more.

Most Americans haven’t seen it coming.

They won’t really know it until they see their retirement funds start vanishing from over-taxation.

And they’ll be left feeling utterly shellshocked.

The stages will roll out like the sudden death of a loved one and the grieving that follows.

First, the denial.

“This cannot be legal. Not in MY America!”

Next up: anger.

“How can the government break its promise to me, after all the work I’ve put in to save for my retirement?”

Then comes the feelings of helplessness.

“If only I had paid more attention, I could’ve kept my nest egg… kept more of my money for retirement… for my kids and their kids.”

And by the time the final stage — acceptance — strikes…

The damage is done.

As I tell my readers, what’s coming down the pike is NOT a pretty picture.

And unfortunately, this new law is already at work.

But there’s still time to protect your money — if you act swiftly.

So again, here’s what I’m doing to help.

I’m sending you a FREE copy of my NEW AMERICAN RETIREMENT PLAN.

In it, you’ll learn the best ways to defend yourself from this imminent Doomsday event.

And I’ll show you the most powerful (100% legal) solutions to every challenge and every obstacle…

Beginning with the 7 “end-around” tactics you can use to dodge Congress’ new law… and help keep the retirement funds you’ve worked so hard to save.

Plus, you’ll discover my entire 4-part plan for creating your own NEW AMERICAN RETIREMENT PLAN…

Including easy-to-employ strategies, techniques, and action steps you can take today to put a shield around your wealth… and get the most out of your retirement.

All Tucked Neatly Into My Groundbreaking Book: The NEW AMERICAN RETIREMENT PLAN (& You Won’t Pay a Single Cent)

The NEW AMERICAN RETIREMENT PLAN — I should tell you up front — isn’t just another new book.

You won’t find it on Amazon, or on the retirement shelf of your nearest Barnes & Noble.

It’s highly specific. And highly personal. It’s the same blueprint I use for my own retirement.

In its pages, I show you everything from how to maximize your Social Security benefits — including getting up to 76% MORE on your monthly payouts PAGE 43…

To how to legally offset the spiraling costs of long-term care (LTC) medical expenses — saving potentially tens of thousands of dollars PAGE 182…

To creating a monthly (and tax-free) income stream to last the rest of your life. PAGE 77

Look, I’ve advised friends and family members to use The Plan for themselves.

I’ve written about many of The Plan’s steps in my Forbes retirement articles.

I’ve even spoken at length about these strategies at retirement and investing conferences across the U.S.

And when I realized Congress was coming after the retirement funds of every American…

I made it my personal mission to create a brand-new approach to retirement…

At a time when American retirees need it most, before this new law — nicknamed the SECURE Act — wreaks havoc on millions of unwitting U.S. citizens.

Here’s a look under the hood of the NEW AMERICAN RETIREMENT PLAN.

The NEW AMERICAN RETIREMENT PLAN goes above and beyond traditional advice, helping solve a lot more of retirement’s biggest issues — like these…

Those are just a few of the action steps I’m recommending in my new book.

I’ve even detailed tips from the estate plans of celebrities including Prince, Tom Petty, Aretha Franklin, Stan Lee, and other high-net-worth names.

The NEW AMERICAN RETIREMENT PLAN is divided into 4 separate sections, each one jam-packed with hundreds more of these kinds of tactics and strategies.

In fact, it’s a complete, easy-to-understand, step-by-step guide anyone can — and should — use to better their retirement finances.

The Plan is like nothing you’ve ever seen, so keep reading to get your copy.

Here’s one of my readers’ favorite chapters…

A Little-known Way to Add Up to

$37,000 to a Tax-free Retirement Account — Every Year

This strategy is completely legal and above board.

And it works even now that Congress’ new assault on your retirement has gone into effect.

It doesn’t end there.

Along with your copy of the NEW AMERICAN RETIREMENT PLAN, I’m also going to give you these 9 Special Reports from my members-only library.

- How to Inflation-Proof Your Nest Egg with ETFs

- Your 20-Minute Estate Plan: Builkding a Lasting Legacy

- The Truth About Annuities — And How to Make Them a Lifetime Stream of Income

- The New Rules of Retirement (recently updated)

- Cashing in Congress’ $350,000 “Retirement Shocker”

- Gimme Shelter: Hidden Real Estate Time Bombs to Avoid

- The IRA Investment Guide: A Roadmap to Avoiding Tax Traps & Penalties

- How to Insure Your Way to a Rock-Solid Retirement

- Keep Your Nest Egg Safe from the IRS Money Grab

Now here’s why I’m doing all this.

Fighting back against the looming Retirement Doomsday is obviously very urgent.

But there’s another reason.

I created this book to raise awareness of… to answer… and to solve…

The #1 Fear About Retirement Today

Every study and survey out there — including with my own readers — reveals the same conclusion.

The single-biggest panic button issue over retiring in America today…

Is the risk of running out of money during retirement.

And if you’re not ready for the effects of this damning new law, the government is going to take a much bigger chunk of your retirement money.

That means you’re likely to run out of it even sooner – which is why I’m rushing you a copy of the NEW AMERICAN RETIREMENT PLAN.

A landmark survey from The Alliance for Lifetime Income shows that a full 80% of non-retired Americans express anxiety that their savings may not provide enough to live on in retirement.

The same study reports that 63% of Americans are unprotected for retirement, meaning they have no source of guaranteed lifetime income outside of Social Security (such as pensions or annuities).

Retirement can last a long time, after all.

So the more thought and effort you put into your retirement plan, the better off you’re going to be.

I’m reminded of a Boston Globe story that said: “As Stocks Swing Wildly, the Future for Baby Boomers Seems Less Secure.”

It’s a stomach-churning read, to be sure.

It talks about the mounting uncertainty of the stock market — on which most retirement plans today hinge — and how it may affect Americans’ financial futures.

Not only does this Boston Globe piece hit on retirees’ biggest fear — outliving their savings…

It also reveals a scary statistic from a new Fidelity Investments report:

While nearly 200,000 Fidelity clients have amassed at least $1 million in their 401(k) retirement accounts…

The average balance in those accounts was a mere $106,000.

Barely more than 10% of what they worked most of their lives to build for and maintain their retirement.

The point here is painfully obvious.

For most Americans, some form of supplemental income will be needed, just to keep a normal standard of living.

Social Security won’t be enough. Not by a long shot.

Don’t just take it from me, though.

Another “Social Security Whistleblower” Comes Clean…

“You Simply Won’t Get Everything, You’ve Been Promised”

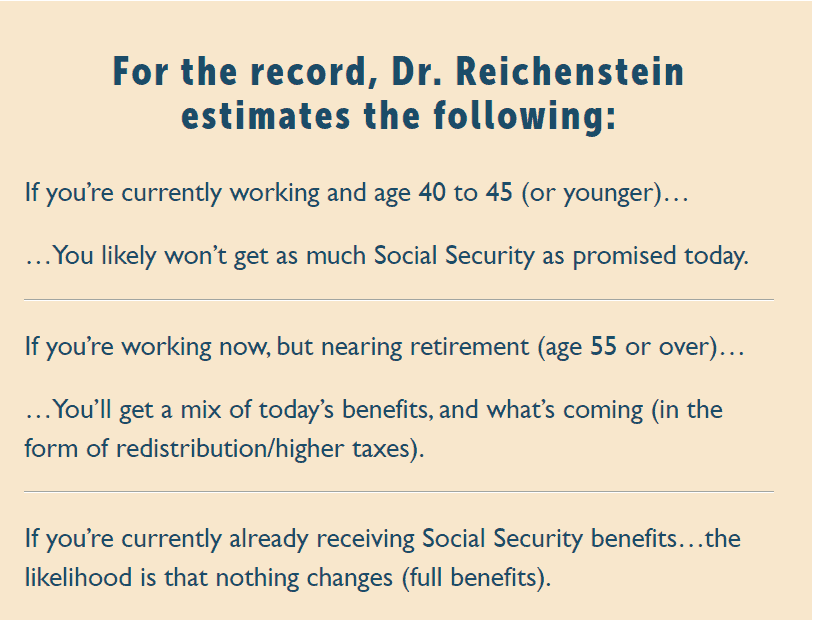

A few months ago I had the good fortune of interviewing one of the country’s leading experts on Social Security reform.

His name is Dr. William Reichenstein.

He’s an Endowed Professor at Baylor University, and also Head of Research at Social Security Solutions.

I wanted to see if Dr. Reichenstein had the same views on Social Security that I do.

And we agreed on just about everything — including the need to blow the whistle on what’s at stake right now for U.S. retirees.

You see, most people — regardless of their education level — fail to fully grasp the complexities of the Social Security system.

There continues to be a whole lot of confusion over the number of benefits… when to take them… and how to maximize them.

The upshot of this confusion?

Too many people leave tens of thousands of dollars on the table during their retirement years. Many leave behind much more than that.

A new study conducted by researchers at Johns Hopkins University found that only 4% of people start collecting Social Security benefits at the most advantageous time.

Most people begin taking benefits as soon as they can… at age 62.

Understandably, for many people that’s out of necessity.

For others… It means thousands of dollars — even tens of thousands — of “wasted income.”

(Another study shows retirees miss out on as much as $3.4 trillion as a result of claiming Social Security too early.)

That’s money Uncle Sam gets to keep for himself.

You’ve paid into this system all of your working life, after all. You deserve to get the most out of it!

What’s worse — Dr. Reichenstein and I both believe that — for many people — the following statement is true about the future of Social Security…

“You simply won’t get everything you’ve been promised.”

Look, neither one of us has a crystal ball.

But we do know this:

The Social Security Trust Fund runs out in 2034…

Which means the government won’t be able to tap into it anymore.

We also know our government never does anything until the last possible minute.

So when that day comes — likely at a midnight hour in late December 2033…

It’ll pretty much be in line with what I’ve been expecting for more than a decade:

A little something insiders like to call “redistribution.”

Politicians will come up with a favorable-sounding name, of course.

Loosely translated to putting lipstick on a pig.

But when it happens, you’ll understand redistribution to mean higher taxes, which means you’ll get fewer benefits.

Probably on the order of 80% of what you should be getting.

Fortunately, my book — the NEW AMERICAN RETIREMENT PLAN — shows how to make the right decisions about Social Security benefits.

In fact, on PAGE 129, I explain the one simple move both individuals AND married couples can take to put an extra $25,000 — or more — in their pockets.

And on PAGE 55, I tell you why the traditional 4% annual retirement withdrawal rate is often completely wrong for people today… and what to do about it.

In short, I’ve put everything you need to create your retirement plan — or to upgrade your current plan — together in one place.

And every time something changes, my team makes sure you have access to the updated version, right away.

You see, there are so many money-saving tips in the PLAN, I consider this book to be…

“Required Reading” for Anyone Over Age 50 (I’m Making Sure You Get Your FREE Copy Today).

Not only will the NEW AMERICAN RETIREMENT PLAN be in your hands just minutes from now…

I’m also extending you a special bonus:

30 days of risk-free membership in my own independent newsletter, Retirement Watch.

It’s a monthly advisory (print and online) I’ve run for nearly three decades, tracking every issue and event that’s critical to retirees.

It’s where I bring together all the techniques and strategies to help everyone in their golden years live their best lives.

*NOTE: I insist on giving all new members a full month to decide if my newsletter is right for you. So if you decide you want a refund at Day 29 — for any reason whatsoever — I’ll promptly return your small membership fee in full.

You’ll even get to keep your copy of my book, the NEW AMERICAN RETIREMENT PLAN.

But I don’t expect that to happen. Most people keep their subscriptions active, because the value they get from membership pays off in spades.

In other words, I cover EVERYTHING, in detail.

If it’s a topic that affects your retirement money… a new tax law, a legal Social Security loophole, or a brilliant way to pay for long-term care in the future…

I’ll share them with you and spell out the pros and cons, so you can decide.

Here’s an example.

When people leave their jobs, they almost always want to know what they should do with their 401(k)s or pensions.

In many cases, they’ll hire a retirement planner or advisor. Not only is this an expensive endeavor, but I’ve found the information people get is too often conflicted and confusing.

My approach is different.

I conduct my own independent and objective research. That’s one reason I have so many loyal, longtime readers.

But I also spend time reviewing other research, which means I know if that research is independent and objective, like mine…

Or on the other hand, if they’re working with Wall Street to help it get more of your nest egg.

Best of all, I explain things in plain English.

And I give my readers all the options… all the possible outcomes… and specific action plans that make it easy to make the right choices to maximize your retirement finances.

I don’t believe in “cookie-cutter” or “one-strategy-fits-all” approaches to retirement planning.

Instead, I identify and spell out whom each strategy is appropriate for and who should steer clear.

The fact of the matter is… retirement planning is always changing, and always will

So it goes without saying, you’ll need to revise your plan. Probably more than a few times.

That’s what we help you do at Retirement Watch.

And if it’s NOT covered on the pages of my newsletter and website…

Or if you have a specific question regarding your retirement plan…

I’ve made it easy for you to ask me your questions directly… through my LIVE conference calls (more on that below).

Here’s another example — one that may still be affecting your finances:

Remember the 2017 Tax Law?

This law was a doozy, and a lot to grasp.

But I read it in its entirety, then told our members all the important changes… BEFORE they went into effect.

One of the worst things about the new tax law?

A lot of people lost money. They lost tax deductions, and it came suddenly, with no warning.

I prepared our members for that. First and foremost, by advising NOT to try specific strategies that the IRS wouldn’t allow.

Another thing I wanted all my readers to understand: today’s low tax rates probably won’t last.

The solution? It’s best to NOT defer income.

In other words, you want to pay taxes at today’s lower tax rates (or you’ll be subject to higher taxes later).

Now, what I just told you goes against conventional retirement planning wisdom.

You see, the first rule of traditional tax planning is to defer income — and taxes — for as long as you can.

But as you’ll see in your free copy of the NEW AMERICAN RETIREMENT PLAN, conventional wisdom doesn’t always pay off.

I did the work. Crunched all the numbers. Then showed it all to my readers and explained that things have changed A LOT.

My research shows you’ll have more after-tax wealth if you pay some taxes now instead of years from now.

Speaking of taxes…

One of the biggest myths about retirement is that your taxes will be lower.

The truth is, despite the income tax rate cuts from the 2017 tax law, your taxes are likely to increase during retirement.

On PAGE 24 of the NEW AMERICAN RETIREMENT PLAN, I’ll show you how to protect yourself from the retiree tax attack.

And when it comes to medical care… well, I’m afraid you’re essentially on your own.

For example, many Americans believe that Medicare, or their employer’s insurance, will cover most retirement medical expenses and long-term care expenses they need.

That’s not even close to the truth.

Fact is, medical expenses will be one of the three biggest post-career expenses for most people, and they’ll only increase as the years go on.

That’s why I keep my readers up to date on the truth about Medicare, Part D prescription drug coverage, long-term care and every other aspect of paying for their medical care.

What we’ve found is that most retirees don’t have this information, so they pay too much out of their own pockets for medical care.

In fact, about 90% of retirees pay more out of pocket than they need to for their medical care.

That’s the kind of advice you’ll get by following Retirement Watch and the NEW AMERICAN RETIREMENT PLAN.

And the money you can save by following my advice?

On PAGE 60 of my new book, you’ll discover The One Simple Move that Can Add $50,000 to your Retirement Account (Without Having to Save Any Extra Money).

So Here’s a Little Background on Me, Bob Carlson…

After getting my law degree and master degree in Accounting from the University of Virginia…

And after passing the CPA exam on my very first try…

I decided I wasn’t meant for the courtroom. Or some accounting office.

Instead, I wanted to use my knowledge to carve out a badly needed niche…

A simple service that could help retirees and pre-retirees help themselves.

By arming Americans with the most up-to-date information, strategies and tactics to get the absolute most out of their retirement.

So I bit the bullet and launched my very own retirement advocacy newsletter from my home office, and with the help of my wife.

To this day, it amazes me to think I’ve written Retirement Watch every single month of every year since 1991.

And if that doesn’t keep me busy enough…

I’m a senior contributor to Forbes.com, as well as an author of three popular books:

The New Rules of Retirement, Personal Finance After 50 for Dummies (with Eric Tyson), and Invest Like a Fox… Not Like a Hedgehog.

Since 1995, I’ve had the privilege of serving as Chairman of the Board of Trustees of the Fairfax (Virginia) County Employee’s Retirement System.

Fairfax is one of America’s wealthiest counties, and as Chairman, I help oversee its investment portfolio valued at over $3 billion.

I also served on the Board of Trustees of the Virginia Retirement System from 2000 to 2005, helping manage a $42 billion pension fund.

And in 1989, I founded the Center for Retirement Security, as a research and collaboration vehicle for retirement finances, investments, taxes, and estate planning.

So I know a thing or two about retirement finances. Still…

I Don’t Like to Toot My Own Horn…

So Here Are Some Nice Things Folks Have Said About Me

So if you’re ready to get the most out of your retirement, here’s…

Everything You Get with Your Retirement Watch Membership…

Your FREE copy of the NEW AMERICAN RETIREMENT PLAN. 190 pages full of actionable ideas for maximizing your retirement finances, starting with my best strategies for sidestepping Congress’ devastating new law — and holding onto your retirement savings.

A 12-month Subscription to My Members-only Retirement Finance Advisory, Retirement Watch. Every month I’ll send you my newsletter, packed with expert answers and simple solutions to make sure you never run out of money in retirement. It’s a powerful, unbiased retirement planning tool to help you eliminate the worry and guesswork.

Access to Retirement Watch’s 5 Easy Chair Proprietary Investment Portfolios: Income Growth, Balanced, Retirement Paycheck, True Diversification, and Sector. I created these in a personalized way so members can meet their goals for income and growth over the long term.

Members-only LIVE Conference Calls. There’s not a single other retirement publisher I know of who takes the time and effort to host these live calls. And my readers tell me it’s one of the greatest perks of membership and best bangs for their retirement buck. On these LIVE conference calls, you ask me your retirement questions directly and I update you on the most pressing retirement issues of the day, along with updates on our five investment portfolios.

Immediate Access to the Retirement Watch Private Website. RetirementWatch.com features the most recent newsletter issue, my free special reports, a searchable archive of all past issues and reports, and many other membership perks.

Full-Time Retirement Services Staff. Here at Retirement Watch, we know when it comes to securing your retirement, it’s easy to make a mistake. That’s why I employ a full-time staff to answer your questions (sorry, no personalized investment advice). Members who write to my team and me directly will get a written response within 48 hours.

Online Retirement Spending Calculator. The first step in retirement planning is to estimate how much you’ll spend, and the second is to estimate how much inflation will affect your spending. My online calculator is comprehensive, making it hard for you to overlook expenses and underestimate the cost of retirement. It also lets you estimate inflation more precisely than other calculators, making it less likely you’ll run out of money in the future.

Ongoing Retirement Education Series. In addition to timely new reports I’ll send you, I also routinely update the reports that affect my members most, including the NEW AMERICAN RETIREMENT PLAN, the New Rules of Retirement, and the New Rules of Estate Planning. Think of these as ongoing retirement coaching, designed to help you make better, smarter, and more profitable decisions about your retirement and my money.

FREE Access to Retirement Conferences Across the U.S. (wherever I’m presenting), which recently included Philadelphia, Orlando, Las Vegas, San Francisco and more.

PLUS Your 100% No-Risk Money Back Guarantee. This gives you 30 days to cancel for a full refund if you’re not completely happy with my advice.

Look, the time has come:

The U.S. government s after your retirement money.

But you don’t have to give it to them!

Not if you act today, and follow the simple steps I’ve laid out in the NEW AMERICAN RETIREMENT PLAN.

To get your copy, you need only to click on the button below.

With your book in hand — and my monthly Retirement Watch advisory — you and your family will be in good hands.

I guarantee it.

Kind regard,

Bob Carlson

Editor, Retirement Watch

Founder, The Center for Retirement Security

P.S. What I’ve just described here is arguably the single most important issue facing retirees today. To protect your nest egg — your IRA, Roth IRA, and 401(k), you need to act now. And the best way to do that is to get your copy of the NEW AMERICAN RETIREMENT PLAN. Remember, you have nothing to lose, and everything to gain.

Click here now to claim your free copy.