The world's appetite for semiconductors has increased big time, as the world is using more and more chips in various applications ranging from smartphones to data centers to cars to video games. IDC estimates that global semiconductor demand could jump 17.3% in 2021, which would be a nice bump over last year's increase of 10.8%.

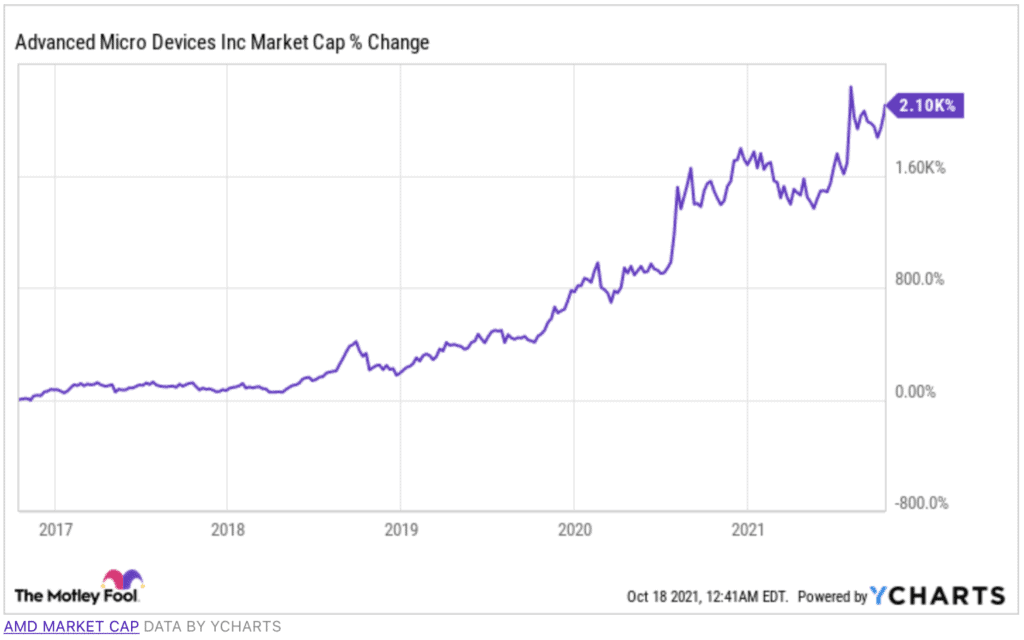

Advanced Micro Devices (NASDAQ:AMD) has been a big beneficiary of this trend as its chips are used in some fast-growing niches, which has triggered impressive growth in the company's top and bottom lines. Investors have rewarded AMD's terrific growth with huge stock market gains, with the tech company's market capitalization jumping 2,100% in the past five years to nearly $136 billion as of this writing.

It won't be surprising to see AMD sustain its hot stock market rally and become a trillion-dollar stock in the next five years. Let's look at the catalysts that could push AMD toward that milestone.

The server processor market could add billions to AMD's revenue

AMD has been consistently taking away share from Intel (NASDAQ: INTC) in the server processor market. According to a report from technology research firm Omdia, AMD's share of the server processor market stood at a historic-best figure of 16% in the second quarter of 2021. The chipmaker has benefited from the increase in demand for its server CPUs (central processing units) from hyperscale cloud service providers such as Alphabet's (NASDAQ: GOOGL) Google.

[Major Trend Alert: The Truth Behind the Global Chip Shortage]

This bodes well for AMD as hyperscale data center deployments are expected to double in the next four years. SK Hynix estimates that there would be 1,060 hyperscale data centers deployed by 2025, which should ensure the sustained growth of AMD's server CPU sales. The chipmaker forecasts that the server CPU market could generate $19 billion in revenue by 2023, and AMD's rising status indicates that it could generate substantial revenue from that market.

Bank of America (NYSE: BAC) analyst Vivek Arya estimates that AMD's server market share could jump to 25% in 2022. If that's indeed the case, AMD could be looking at nearly $5 billion in annual revenue from the server chip market in the next couple of years, given the potential size of the end market discussed above. Now, the server market had accounted for 20% of AMD's total revenue of $3.85 billion in the second quarter, indicating that this market is clocking an annual revenue run rate of around $3 billion.

As a result, the server market looks set to become a substantially bigger business for AMD and help it sustain the rapid growth of the enterprise, embedded, and semi-custom (EESC) business that produced 42% of the total revenue in the second quarter. The EESC business had recorded 183% year-over-year revenue growth to $1.6 billion during the quarter. The good news is that this segment has another solid tailwind at its back that could complement the server business's massive prospects.

Gaming consoles are going to be a multi-year catalyst

The demand for AMD's semi-custom chips has shot up remarkably since last year as it is supplying chips to Sony (NYSE: SONY) and Microsoft (NASDAQ: MSFT) for their gaming consoles, a trend that's likely to continue as the new consoles are still at the beginning of their lifecycle. Sony, for instance, had sold 4.5 million PlayStation 5 (PS5) consoles last year. It expects that figure to increase to nearly 15 million this year. By 2024, Sony is expected to sell almost 42 million consoles annually, indicating that the robust demand for its semi-custom chips is here to stay.

[Don’t Miss: Former Tech Executive Issues Urgent Plea]

On the other hand, Microsoft is expected to sell around 12 million units of its new Xbox consoles this year. That figure is expected to jump to 37 million units a year by 2024 as per third-party estimates. Throw in the fact that AMD has added another console customer to its portfolio in the form of Valve, and it is safe to assume that the semi-custom business's growth is here to stay for a long time to come and substantially boost the company's revenue.

Gaining share in a multi-billion-dollar market

AMD gets most of its revenue from the computing and graphics segment. This business had recorded 65% year-over-year revenue growth in the second quarter to $2.25 billion, accounting for just over 58% of the company's top line.

AMD is benefiting from the strong demand for its Ryzen CPUs in this segment that's leading to an increase in market share and average selling prices. The company had just 9% share of the desktop and laptop CPU market in 2017, which went up to 17% in 2019. Even better, AMD saw a 6% increase in the average selling prices of its CPUs in 2018, followed by a bigger increase of 19% in 2019 which shows an improvement in the company's pricing power.

According to a survey of users on popular game distribution platform Steam, AMD has reportedly cornered 30% share of the PC (personal computer) CPU market already. With a monthly active user base of 120 million, Steam's survey indicates that AMD has continued gaining share against Intel in the CPU space. This is going to be a massive tailwind for AMD, as more share gains in this space could give AMD a big shot in the arm in the long run. That's because AMD sees a $32 billion addressable opportunity in the PC market.

In all, AMD's several catalysts are likely to help the company record consistently impressive growth in its top and bottom lines in the coming years.

In fact, analysts are looking at 32%-plus earnings growth annually for the next five years. All of this could ensure sustained growth in AMD's stock price and market cap in the future and eventually help it become a trillion-dollar company on the back of the multiple growth drivers it is sitting on.

[“The Tech Shock” – Stocks to Buy and Companies to Avoid During the Global Chip Shortage]

Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool's board of directors. Bank of America is an advertising partner of The Ascent, a Motley Fool company. Teresa Kersten, an employee of LinkedIn, a Microsoft subsidiary, is a member of The Motley Fool's board of directors. Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool owns shares of and recommends Advanced Micro Devices, Alphabet (A shares), Alphabet (C shares), and Microsoft. The Motley Fool recommends Intel and recommends the following options: long January 2023 $57.50 calls on Intel and short January 2023 $57.50 puts on Intel. The Motley Fool has a disclosure policy.