PRESENTED BY STANSBERRY RESEARCH

Washington Economist who called Lehman Bros. collapse says…

The Banking Network Behind EVERY Major Economic Calamity (1907, 1929, 1998, 2007)

Is About to Blow Up Again

![]()

Hi, my name is Dan Ferris. I’m the Senior Analyst at Stansberry Research.

We’re a financial research firm founded 24 years ago for regular folks who don’t trust Wall Street and want to manage at least some of their own money.

And… we’re one of the few firms in our industry that publishes an audited track record of all our recommendations, every single year.

Today I’ve traveled across the country to the heart of Washington, D.C., because I’m terrified the mainstream press and most “financial experts” are sending Americans down a very dangerous path of complacency.

And so I have a warning:

I believe the next 2 years will be some of the most difficult in American history – everything you have is now at risk.

I’ll explain why this is true, and the exact steps I believe you should take.

And I want to start by sharing THE MOST IMPORTANT SECRET for surviving this time. The best way to explain it is with a real life example. This secret helped a small group survive the greatest disaster in Wall Street history…

It was a clear fall day, not too long ago, when Rick Rescorla went to work on Wall Street, just as he’d done for more than a decade.

The night before, a cold front swept through Manhattan. A bright, cloudless, and sunny day followed.

Years earlier, Rick Rescorla served as a soldier in the Vietnam War, where he earned a Silver Star, a Bronze Star, and a Purple Heart.

When he returned home, Rescorla landed a job as head of security for Morgan Stanley.

And as you’ll soon see, Rick Rescorla was the best investment Morgan Stanley ever made.

His insights and ideas transformed the future of the company… but probably not in the way you might imagine.

On the job for more than a decade, Rescorla was a visionary leader who was not afraid to take action, even as others were lulled into complacency.

Each year, for example, Rescorla put thousands of Morgan Stanley employees through rigorous drills on what to do in the event of a crisis.

This was highly unusual on Wall Street.

But Rescorla did it because he knew that in any crisis, no one would come to their rescue. They had to learn to take care of themselves.

Now Rick, remember, was a soldier, but he worked with investment bankers, many of whom had big egos. Many of these folks didn’t appreciate Rescorla’s “drills”… which took time away from “deal-making” and trading.

As one executive reports:

“[Rescorla] was very serious about making sure everyone came out to the drills. We used to say, ‘Well, it’s the sergeant doing the drills again.’ It was kind of repetitive. There were times when I just sat in my office and the fire marshal would come by and say, ‘No, you gotta go.’”

Then one early fall morning, all of Rescorla’s drills paid off…

Sitting at his desk, Rescorla heard an explosion, looked out the window, and saw a nearby building burning.

Soon, an official came over the public address (PA) system, explaining how there was no “reason to panic—and everyone should remain seated.”

But Rescorla knew better.

And because he’d spent hundreds of hours training employees to ignore the “official” advice, and to take matters into their own hands, Morgan Stanley employees followed Rescorla.

With his bullhorn, walkie-talkie, and cell phone in hand… Rick Rescorla systematically moved Morgan Stanley employees to exit via the stairwells.

That day, more than 2,500 employees and visitors were following the former soldier’s evacuation plan.

But then, the situation got worse.

A second explosion rang out, this one a lot closer.

It occurred in Rescorla’s building, about 40 floors above their heads. It shook the entire building. Dozens of employees fell to the ground.

It was September 11, 2001.

World Trade Center Tower 1 was hit by a commercial plane at 8:46 a.m.

Just 17 minutes later, at 9:03 a.m., terrorist hijackers flew a second plane into Tower 2, where Rescorla was trying to evacuate 2,500 people.

But Rescorla didn’t panic.

He grabbed his bullhorn and spoke calmly: “Stop. Be still. Be silent. Everything is going to be OK. Remember, you’re Americans.”

Rescorla did this because he understood how in any crisis…

Most people are prone to waste extraordinary amounts of time in a phase of Denial and Procrastination, before ever taking action.

So Rescorla repeated his orders.

He even sang childhood songs to prevent employees from lapsing back into the Denial and Procrastination phase.

Rescorla knew that in any crisis, most people freeze. Our brains attempt to convince us that, “Nothing is out of the ordinary… and everything is going to be OK.”

In other words: In every type of crisis… People move much too slowly.

Get this…

According studies, the average Trade Center survivor waited six minutes before heading downstairs. Some waited 45 minutes.

Despite the fire, smoke, the smell of jet fuel, and swaying buildings, an estimated 1,000 people took time to shut down their computers. Others made phone calls and gathered belongings.

But because of Rick Rescorla and his training, most Morgan Stanley employees were able to push quickly through the denial phase and spring into action.

The company was the biggest tenant in Tower 2, occupying 22 floors. Incredibly, all but 13 of 2,700 employees made it out alive that day.

Unfortunately, Rick Rescorla was not one of them.

After escorting thousands to safety, Rescorla learned there were some folks left behind.

So he headed back in, just before Tower 2 collapsed.

I’ve told you Rick Rescorla’s story today for one simple reason…

He’s truly an American hero we can all learn from—especially right now.

You see, in America today, while our physical lives are not yet in danger—we have definitely entered an extremely dangerous new crisis, which most people are taking far too long to recognize.

Just think about what’s happening right now…

- How can things be back to “normal” in our financial system when interest rates shot up 2,000% (at the fastest rate in history) and the Fed reports 722 U.S. banks have LOST 50%+ of their working capital?

- How can the situation be “normal” in America when people are stealing more than $1 billion per year from Target—almost doubling last year’s total.

- How can everything be OK when the owners of many of our biggest hotels and office buildings (in the richest cities like New York, LA, and San Francisco), are simply walking away from their properties and mortgages, just like homeowners did back in 2008?

- How can things be “normal” when more than 600 of America’s biggest companies can no longer afford to pay even the interest on their debts?

- And how can everything be “OK” when U.S. employers just announced a 287% increase in job cuts compared to a year ago?

Still, even in the face of all this evidence, most Americans are in complete denial that anything significant has changed in our economy and financial system.

And the truth is, it’s not their fault.

I estimate 95%+ of Americans are in denial now because we simply have not experienced anything like this in more than 40 years.

For folks under the age of 60, inflation and higher interest rates are little more than “theoretical concepts.”

So I want to say this as simply and clearly as I can…

Higher interest rates and higher inflation are the most insidiously brutal developments of our time.

Both will almost undoubtedly go much higher from here (I’ll explain why this is inevitable), and will cause extraordinary damage over the next two years.

The sad thing is, the denial trap most are falling into today is the exact same trap that ensnared millions during America’s last Great Inflation (1968 to 1982).

Back then, people thought inflation and higher interest rates were beaten on THREE DIFFERENT OCCASIONS before both came roaring back, causing massive damage.

Everyone thought inflation was done here… here… and here…

But they were wrong. They were in denial. And it cost them a fortune.

As journalist Robert Samuelson writes about that period: “The Fed stepped ‘hard on the monetary brake’ in 1966, 1969 and 1974… [but] each time the Fed relented too quickly before inflation was broken.”

And after each “false victory,” stocks rose, then got hammered, falling an average of 32% each time.

It’s identical to what’s happening right now!

Nearly everyone in the financial world… professionals and regular folks alike… see stocks rising and inflation falling… and they believe our financial troubles are over.

Many are even excited—they think a new bull market has begun.

But this is the exact same denial trap that caused devastation in our last Great Inflation.

And as Warren Buffett’s investing partner Charlie Munger says:

“Denial is a common way for people to go broke.”

Today I’m going to show you what’s really coming next.

I’ll show you how inflation and higher interest rates will inevitably come roaring back. Most importantly, I’ll show you how these problems are causing a Shadow Banking Network to make some devastating decisions about your future.

This is the same network that’s caused ALL of America’s biggest economic calamities (1907, 1929, 1998, 2007).

And now they’re about to do it again, as the next phase of this crisis unfolds.

I’ll name names and show you everything you need to know.

The most important takeaway I hope you’ll get from today is this: What’s really happening in the economy and the markets right now is NOT what’s being reported in the news.

So… if you believe the worst is behind us… if you think inflation and higher interest rates have peaked… and that a new bull market has begun…

Consider this your final wake up call.

I want to break you from the Procrastination and Denial Phase, just as Rick Rescorla did when he saved so many lives on 9/11.

For starters, here’s the first thing I want you to recognize…

The Trillions of Dollars in Losses

Almost EVERYONE Is Hiding

Today, most Americans are in denial, either because they don't understand economic theory, economic history… or both.

Take the massive damage that’s already occurred — and the greater damage still to come — from “unrealized losses,” for example.

I’m sure you’re familiar with that term.

For example…

If you buy 1,000 shares of stock at $10 a share, it costs you $10,000.

But if the $10 share price falls to $2, you’re now sitting on just $2,000… so you have $8,000 in “unrealized losses.”

Maybe the price will come back… or maybe it won’t — but you’re definitely $8,000 poorer.

This is exactly how Silicon Valley Bank went broke when forced to liquidate billions in “unrealized losses.

And this is how 722 U.S. banks have LOST 50%+ of their capital, because of unrealized losses on supposedly “safe” investments like U.S. Treasuries.

And here’s the truly terrifying part…

It’s not just banks sitting on extraordinary losses — it’s all kinds of businesses in every industry.

But because of accounting rules, most businesses (unlike regular banks) don’t report their “unrealized losses”— they get to keep the original purchase price on their books.

But anecdotally… we’ve dug into a handful of firms, and the losses are astonishing…

Take insurance companies…

You’ve probably heard of USAA. They recently booked a $1.3 billion loss — their first in 100 years. Net worth declined more than 30% and they had $10.5 billion in “unrealized losses.”

Then there’s Lincoln National, which had unrealized losses of $9.6 billion in its securities portfolio as a result of rising interest rates.

Again… so far… only a few of these “unrealized losses” have popped up anecdotally, but what you have to realize is that these unreported losses are EVERYWHERE in the financial industry…

Ares Capital, for example, is one of America’s biggest Business Development Corporations. They’re sitting on $184 million in unrealized losses… again… primarily because of rising interest rates.

A mortgage company called Cherry Hill reported “unrealized losses” of more than $12 million.

And these massive unrealized losses aren’t just in the financial sector… they’re everywhere…

Century Aluminum had “unrealized losses” of roughly $48 million.

John Deere had $94 million in unrealized losses.

Microsoft had over $2 billion worth of unrealized losses in U.S. Treasuries. Google had more than $2 billion in Treasury losses… and Apple had more than $13 billion in total “unrealized losses.”

Amazon had $800 million in total unrealized losses. Facebook had $1.6 billion in unrealized losses by holding U.S. government and corporate debt.

And most incredibly — even the supposed “safest stock in America,” Berkshire Hathaway, reported a whopping $43.8 billion in “unrealized losses” in a single quarter.

Are you starting to see why big problems lie ahead for the markets and the economy?

We’ve wondered who was dumb enough to lend the government money for 30 years for essentially no return…

And now we’re finding out, as the value of these “investments” are destroyed and the results finally leak out to the public.

As a result, we are headed for a “Write-Down Bonanza”… as my friend Chris Weber calls it… as hundreds of firms are forced (in the coming months) to “recognize” their incredible losses.

Right now… most of these companies are still in the “Procrastination and Denial” phase, just like most investors.

They are “sitting and praying”… hoping their losses will disappear (if inflation and interest rates go way back down).

But I believe, despite the temporary fall in both inflation and interest rates, both will only go higher from there. Remember, we saw this exact scenario during out last big inflation.

And keep in mind: There’s a huge price to pay for what’s happened over the past 15 years in our financial system.

The Fed artificially suppressed rates for nearly two decades… and at the same time, expanded the U.S. monetary base (the amount of currency in circulation and bank reserves) nearly 10-fold from $830 billion to over $6 trillion.

In other words, the Federal Reserve created more than $5 trillion out of thin air in a very short period of time!

It’s inconceivable to think we can “fix” those mistakes with a short series of rate hikes that top out around 6%. There’s still a huge price to pay for all the debt taken on at artificially low rates.

The eventual write-downs on these losses will send shockwaves through the markets—stocks could easily drop 40% from today’s levels.

And the “unrealized losses” are only a small piece of the problem.

In fact, there’s an even bigger problem on the horizon, which almost no one is talking about…

The Refinancing Crisis Of The

Century Has Just Begun…

In recent years, individuals, businesses, and governments all borrowed way too much money, at artificially low rates.

And now, these loans are coming due. So they’ll have to refinance at rates that could be 10 times higher than what they’re currently paying!

A front-page Bloomberg story sums it up this way…

For starters, total corporate debt is at record highs, now $11 trillion (not counting financial institutions).

What’s crazy is, not only did the Fed artificially suppress interest rates… they also encouraged even MORE borrowing by taking the unprecedented step of directly lending to businesses and purchasing corporate bonds!

I predict these mistakes will go down as the worst Central Bank decisions in history… even worse than their moves during the Great Depression and the Great Inflation of the 1970s.

Now, these debts are coming due. And the consequences over the next two years will be brutal…

- Verizon, for example, has about $25 billion in debt coming due in the next few years, with interest rates as low as 0.75%.

But to refinance at today’s rates, they’ll probably pay more than 8 times that amount… and it could mean a BILLION dollars is wiped away from their profits.

- John Deere has about $20 billion in debt coming due in the next two years. They’re likely to pay twice as much to refinance… it could mean a $500 million-dollar hit to their bottom line.

- Ford has $75 BILLION coming due. It could cost them billions in extra money to refinance.

- General Motors has $58 BILLION coming due over next two years. It could mean a $1.7 BILLION hit to their bottom line.

- Warner Bros. has so much debt to refinance, they could take a $120 million hit.

And just like the “unrealized losses” I described earlier, the refinancing disaster will affect thousands of companies, in every sector.

- In the next two years, T-Mobile has nearly $10 billion coming due… Caterpillar has $13 billion… Dell computers has more than $10 billion… Boeing has $10 billion… Marriott has $2 billion… Disney has $5 billion … the list goes on and on and on…

CVS… Walmart… McCormick Spices… Medtronic… Starbucks… Colgate… Apple… UPS… Home Depot… Pepsi… Amazon… they all have billions and billions of debt to be refinanced at rates that could easily cost 10 times what they’re currently paying.

And over the long term, it gets even worse. Companies like ExxonMobil, General Mills, and Netflix will be forced to refinance 99% or more of their debt.

I mentioned earlier how more than 600 out of America’s biggest corporations already can’t afford even the interest payments on the debts. It’s only going to get worse from here.

Of course, the firms I just described are America’s biggest and best businesses.

These businesses aren’t likely to go bankrupt — but they will take huge hits.

Remember, the “Write-Down Bonanza” is coming.

But for smaller companies, with less cash and limited access to new credit…

It could mean complete collapse or bankruptcy, because they simply won’t be extended the credit they need.

In fact, already this year we’ve seen the highest rate of corporate bankruptcies in more than a decade.

The numbers are double what we saw last year… and bankruptcy rates are only going higher from here.

Many small firms will be crushed…

You’ve probably heard of Lions Gate, the film and TV studio behind Rambo and the Hunger Games series, for example.

They’ve got $1.4 billion in debt coming due in the next two years, and at current rates, it’s going to cost the business an extra $110 million. In other words, their earnings will likely fall 25%. They’ll be lucky to survive.

Or look at Six Flags…

They’ve got a billion dollars in debt coming due in the next two years, and it’s likely to cost them an extra $30 million when they refinance… a 20% hit to their net income.

Or take Piedmont Office Realty…

The company’s stock has fallen around 60%. It’s worth about $800 million today… but they have $940 million in debt coming due in the next 2 years!

If by some miracle they can refinance, it’ll be at much higher rates, which could cost an extra $54 million per year.

This is a slow-motion train wreck of a business… Yet many of the biggest money managers in the world still hold millions of shares… Vanguard, Charles Schwab, BlackRock, Fidelity, and more.

And Piedmont is not alone… Hundreds of publicly traded companies are in a similar position.

And private companies (those not publicly traded) are in even worse shape, because they have even less access to credit. As Bloomberg reports:

I’ll show you in a minute exactly how I believe many private companies will soon go under.

But for now, I want you to remember this…

Higher interest rates and higher inflation are just at the start of inflicting enormous damage. We are still just in the first or second inning of this New Era.

To make matters even worse, families and governments are facing the same refinancing problem too…

Payments on mortgages, credit cards, and personal loans (which are all at record highs) are going much, much higher in the years to come. U.S. credit card debt just hit a record high… nearly $1 trillion… and those interest rates are soaring.

U.S. household debt just hit record highs too… a whopping $16.9 TRILLION! And it’s all going to have to be repaid at much higher rates.

Cities and towns all over America are in the same boat… getting crushed by inflation and higher interest rates…

- New York’s mayor has called for massive cuts because of a $2.9 billion shortfall next year.

- Oakland is facing the largest deficit in the city’s history ($345 million).

Chris Goodman, municipal finance expert says:

“Everything has become more expensive… and revenues are just not growing at the same rate… We have not experienced a level of inflation like this in 40-45 years. …There’s basically no one doing state and local finances in the trenches that understands how any of this works. ”

And that’s the main takeaway I hope you’ll get from my work today:

Everyone is in denial, because very few understand the devastating consequences of higher rates and higher inflation.

As Nassim Taleb recently told CNBC:

“Lowering rates to zero for 15 years made no sense… we have a generation of financiers who don’t know what interest rates mean… so welcome to a New Era.. we’re going to pay the price.”

Our federal government is going to pay an enormous price too…

Did you know that about 30% of our national debt (more than $7 trillion) has to be refinanced in the next 12 months?

And as this debt is rolled over, the new rates will likely be 100% higher than what we pay now.

We already pay as much in interest on our debt as we spend on ALL our military and defense (about $1.3 billion per day). And just look at the crazy amount we will soon be paying just in interest on the money the federal government borrows…

I hope you’re beginning to see now why rising rates and rising inflation are going to cause enormous problems over the next two years.

But wait…

Can’t the Fed just wave their magic wand… and go back to the conditions we had for the previous 15+ years?

Unfortunately, that’s impossible…

The Huge Misconception About Interest Rates…

When you look at what’s happening today, and compare it to the last big inflationary period (1968-1982), the similarities are staggering…

Just like today, the years leading up to late 1968 saw stocks soar 350%. Back then, just like today, people simply expected stocks to rise continuously, with only brief pauses.

But 1968 (just like 2022) was a turning point.

That’s when the inflation rate doubled in two years, and stocks fell more than 30%.

Over the longer term, stocks went absolutely nowhere for more than a decade, just grinding up and down.

Along the way there were stock market rallies just like we’re seeing today (some as high as 50%)… but they were short-lived, and anyone counting on stocks got hurt.

Adjusted for inflation, stocks peaked in 1968 and took 24 years just to get back to even.

And as I mentioned earlier, people thought inflation was beaten on three different occasions… before it came roaring back again.

- First folks thought inflation was done in the mid 1960s… but as the economy reaccelerated, inflation more than doubled by 1969.

- Then after the wage-price controls of 1971, inflation dropped, before soaring to more than 12% by 1974!

- Finally, in the last inflation “fake-out,” it fell in 1976 — before skyrocketing to 13.3% in 1979.

Today, everyone says… “Oh… look at the 1980s… inflation and interest rates spiked, then quickly came back down.”

But the period we’re in today isn’t comparable to the 1980s — that was the END of the last big inflationary period.

The period we are in today is comparable to the early 1970s… which was still the BEGINNING of the last Great Inflation. Like I said, we’re only in the first or second inning of a 9-inning game.

That’s a lot of numbers I’ve thrown out at you, I know… and if you want to see the sources for these figures and all the data presented here, see our details & disclosures page, linked to at the bottom of this page.

The critical point I want you to take away from all of this is that today we are here on this chart!

There’s still much more pain to come. It’s impossible to say how many inflationary waves there will be… but I’d bet anything it will NOT be just one.

And of course, the “experts today are saying the same things today that the “experts” said back then…

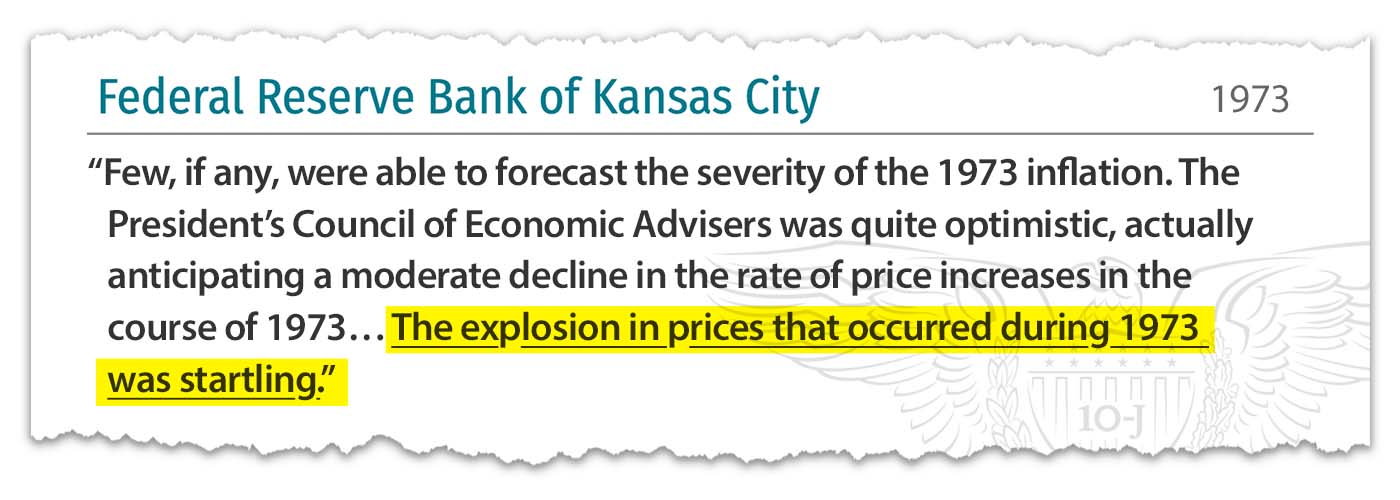

Here’s what the Kansas City Fed reported in December of 1973 in their forecast for 1974:

But guess what…

They were completely wrong… Inflation actually soared the next year to more than 12%!

In fact, the experts weren’t wrong just one year… they were wrong EVERY year for an entire decade…

As Charles Schultze, director of the Bureau of the Budget under President Lyndon Johnson, said about the 1970s:

“In every single year of the 1970s, the consensus forecast [of inflation] made late in the previous year understated the actual value of inflation.”

It’s practically identical to what’s happening right now!

Remember: The Fed made the biggest blunder in U.S. monetary history (even bigger than their blunders during the Great Depression and the Great Inflation of 1970s), by artificially suppressing rates for nearly two decades…

And at the same time, they created more than $5 trillion new dollars out of thin air.

It’s inconceivable to think they can quickly “fix” those terrible mistakes with one short series of rate hikes that top out around 6%.

The Fed… the “experts”… the mainstream press… I’m convinced they will ALL be wrong again over the next few years… just like they were wrong EVERY SINGLE YEAR for a decade in the 1970s…

And now you see this happening already right now…

Back in 2021, Bloomberg wrote:

Well, guess what?

Here we are and inflation rates have been 50% to 100% higher than the “experts” predicted for both years.

Do you really think they are going to get it right over the next few years? They have a perfect track record of being WRONG nearly every time!

The thing is, most Americans think the Fed has complete control over interest rates, but the truth is, they control only the very short-term rates. Long-term rates are set by the market.

For example, in 1981, interest rates on 30-year Treasury bonds averaged about 13.5%. And mortgage rates were 15%.

We hit those rates because people lost faith in the government’s ability to control inflation. Investors in the market were protecting themselves against future price increases of 10% a year or more.

And that’s what will ultimately happen today—interest rates and inflation will soar again.

And it will only end, just like it did in the 1980s, with a massive recession.

Before the last great inflation ended in the early 1980s, bankruptcies hit the highest rate since World War II… then doubled again the next year.

Prices for everything from Hershey’s bars to Campbell’s soup… Cornflakes to a McDonald’s Hamburger… soared by more than 150%.

Many truckers had to agree to pay cuts or lose their jobs altogether. Can you imagine the grief pay-cuts in any field would cause today?

Unemployment skyrocketed to more than 10%. Imagine what would happen if 20 million Americans lost their jobs over the next few years!

In short, the entire economy was flipped upside down…

And that’s exactly where we are headed today.

The big question, of course, is what will be the next shoe to drop?

I believe I have the answer…

The Shadow Banking System Behind Almost EVERY Major Economic Calamity (1907, 1929, 1998, 1982, 2007) Is About to Blow Up Again

When you look back at the biggest financial calamities in America…

1907… 1929… 1982… 1998… 2007…

They can all be traced back to the exact same place.

They each began in what’s known as a “Shadow Bank.”

You’ve probably heard this term before. It’s not as complicated as it sounds.

“Shadow Banks” are the institutions operating on the periphery… or in the “shadows of” regular banks.

These institutions behave much like ordinary banks, but with a few critical differences:

- First, they aren’t regulated like ordinary banks.

- Second, they typically create riskier financial instruments, while avoiding regular banks’ capital requirements.

- And finally, they’re A LOT LESS LIKELY to be bailed out by the government. There’s no FDIC insurance, for example.

A recent Washington Post article sums it up this way:

We’re talking about hedge funds, private equity firms, investment trusts, business development corporations, mortgage lenders, insurance companies, and money market firms… just to name a few.

And the incredible thing is, when you study economic history, you find that the Shadow Banking System is ALWAYS where the biggest disasters start.

In fact, all of America’s biggest economic calamities follow a similar pattern. (The same pattern that’s unfolding right now.)

Take 1907, for example.

This was the twilight of the “Gilded Age.”

Electricity was transforming our world. The U.S. economy grew faster in one decade than at any other previous time in American history.

This led to rampant speculation, soaring asset prices, and rising interest rates, as the Bank of England and other central banks raised rates as much as 70% to deal with the speculative stresses.

And here’s the most important part to remember…

This financial disaster, like all the others to come, followed the same exact script…

- First, massively inflated assets and rising interest rates provide the fuel…

- Then a spark from the highly-unregulated Shadow Banking Sector lit the fire.

In the fall of 1907, that “spark” came from Shadow Banking firms called “Trust Companies.”

There were more than 1,300 Trust Companies in America back then, which invested in riskier and less liquid assets. But also paid higher rates and held less money in reserves than ordinary banks.

In October of 1907, news broke that the Knickerbocker Trust Company was involved in copper speculations gone wrong.

And as historian Sean Carr writes:

“By day’s end, widespread fear and uncertainty would spread like a brush fire.”

More than 1,000 people lined up to withdrawal their money from one trust. One stock exchange halted trading as prices collapsed. And cash simply disappeared…

Get this: 2,000 new safe deposit boxes were rented in New York, where customers withdrew savings and literally locked it all up.

Overall, hundreds of millions of dollars were withdrawn from the system and hoarded away. The stock market fell 43% in roughly a year, and many banks closed for good.

Something similar happened at the end of the Roaring 1920s…

Again, the script was the same…

The Dow stock index went up six-fold in the years before 1929.

Then just like in 1907, rising interest rates and inflation provided the fuel.

Next came a spark from the Shadow Banking Sector…

This time it was stock brokerage offices, which more than doubled before the 1929 crash, and “Investment Trusts,” which grew by more than 1,770% over roughly the same period.

These Shadow Banks lit the fire by offering “margin accounts,” which required as little as a 10% down payment to buy stocks.

As historian John Turner concludes:

“The quantity of outstanding broker loans in the autumn of 1929 meant any sufficient fall in prices would lead to a significant number of margin calls. This in turn would force traders to liquidate, depressing prices further.”

Again… rising rates and inflation provided the fuel…

Then a problem in the Shadow Banking sector lit the spark, leading to one of the biggest financial calamities in American history. Stocks dropped 90%. Unemployment hit 20%.

It nearly happened again in the late 1990s…

Soaring asset prices and rising rates (which went up 60% in two years in the late 1990s) provided the fuel…

And a Shadow Bank called Long-Term Capital Management (LTCM), which used massive leverage to control as much as 5% of the world’s bond market) went bust, setting off a chain reaction.

Treasury Secretary Robert Rubin said at the time, ”the world is now experiencing its worst financial crisis in 50 years.”

Almost every big financial firm lost a small fortune: Merrill Lynch, Bankers Trust, UBS, Credit Suisse First Boston, Goldman Sachs, and Salomon Smith Barney, just to name a few.

The same thing happened again in 2007…

Interest rates soared more than 700% between 2002 and 2007…

And assets skyrocketed. Some areas (like Miami, Las Vegas, and Phoenix) saw house prices soar more than 100%.

Shares of the largest homebuilder (D.R. Horton) soared 1,300%.

Rising rates and asset inflation provided the fuel… then Shadow Banks provided the spark.

Dozens of Shadow Banks created and sold “Mortgage Backed Securities.” They didn’t care much about the quality of these “investments,” because they figured it would be someone else’s problem once they were sold.

And when prices collapsed, it nearly brought down the entire financial system.

One thing to keep in mind here…

Most Shadow Banks are businesses you’ve probably never heard of… but many of these firms are hiding in plain sight.

Lehman Brothers, for example, was probably the most famous Shadow Bank of this era.

In 2008, Lehman had billions of “unrealized losses,” the exact same problem plaguing many businesses today. Eventually, their “Write-Down Bonanza” took place as they were forced to recognize $6 billion in losses.

I warned my readers about all of this back in April of 2008, by the way.

I even showed folks how to profit by betting against Lehman five months before it went bankrupt. This resulted in an 82% return for folks who followed my recommendation.

Most people, of course, lost a fortune in this crisis, as stocks fell 50% in 18 months, 9 million people lost their jobs, and nearly 10 million Americans lost their homes.

And as a Philadelphia Federal Reserve paper concluded:

And that brings us to today…

Here's What The Next Phase

Of This Crisis Will Look Like

We’ve seen interest rates skyrocket 2,000% since the Fed started hiking, and we’ve seen inflation soar.

We saw stock prices fall… then rebound in a big way, just like what happened in the 1960s and 1970s.

And by now, you already know exactly what’s coming next:

A “new” problem in the Shadow Banking space will likely spark the next big wave of today’s crisis.

And here’s the scary part.

The situation today is much worse now than it was in 2008, because low rates pushed so much money into the Shadow Banking System as people chased higher yields. Today, Shadow Banks now make up roughly HALF of all the world’s financial assets!

And remember…

Unlike ordinary banks, Shadow Banks don’t report their “unrealized losses”… their default rates… or how much money they are going to lose when they have to refinance loans at much higher prices.

In other words:

We still basically have no idea yet how bad the situation is in America’s Shadow Banking Sector.

As Bruce Flatt, the head of one of America’s biggest Shadow Banks (Brookfield Asset Management), admits: “What we do is behind the scenes. Nobody knows we’re there.”

I conservatively estimate the problems in Shadow Banks are at least twice as bad as the regular banking system (where there are still $600 BILLION in unrealized losses).

In short: There could easily be a trillion dollars in unrealized losses and new interest rate expenses in Shadow Banks today.

And while it’s impossible to say exactly where the next volcano will erupt, I’m confident we’ll see several financial catastrophes in the Shadow Banking System over the next two years.

For example…

The “Private Debt” market is one part of the Shadow Banking system just waiting to detonate.

Private Debt, by the way, refers to money lent or borrowed by privately held companies. It usually involves non-bank institutions (Shadow Banks), making loans to private companies or buying those loans on the secondary market.

The important thing to remember is this: Private debt is the riskiest of the risky debt out there today. Companies seek it because they can’t borrow elsewhere.

And this sector has exploded in recent years, now topping $1.4 trillion.

Defaults in this space are already soaring, but only insiders know what the real totals will be.

This I assure you: We’ll find out soon… and a disaster in the Private Debt markets is coming… but you won’t know exactly where or who it will hurt until it actually explodes.

But the Private Debt disaster is going to be nothing compared to…

Where I Believe The Next Phase Of This Crisis Will Begin…

It won’t surprise you to hear that owning office and retail buildings is a terrible idea right now.

Covid shut down many offices and stores, which aren’t coming back any time in the next decade, if ever. And renters have already stopped paying rent at extremely high rates.

More worrisome, we are starting to see HUGE problems in this space, especially among the “Shadow Bankers,” who finance and own so many of these properties.

Columbia Property Trust (a Shadow Bank), for example, recently defaulted on $1.7 billion in mortgages on seven “trophy” properties, including the former headquarters of the New York Times.

Shadow Banker Brookfield Corp (one of the biggest property owners in the world, and another Shadow Bank) defaulted on two downtown Los Angeles skyscrapers.

And in San Francisco, the owners of two of the biggest hotels stopped making mortgage payments. The same goes for the owners of one of the city’s biggest malls.

They are all simply handing over the keys and walking away. Their losses will likely tally in the billions.

This year, $92 billion in office mortgage debt from Shadow Banking lenders is coming due. And it couldn’t come at a worse time – when rates could be as much as 10 times higher than a few years ago.

Some estimates are that 70% of office buildings are now doomed.

The official numbers show that 20% of offices are now vacant — a number that’s already higher than the 2008 crisis, and is probably wildly underestimated.

If you’ve been in any American office building in recent months, you know what I mean.

While 80% of office space is currently being rented, only a fraction of that space is actually being used.

This is why just about every major company, municipal government, and even non-profit is trying to sell, sub-lease, or get out of their current office lease.

And it’s why Chris Hansen of Valiant Capital believes massive defaults in commercial real estate are coming… which will touch off what he calls:

The “worst economic collapse in more than a decade… or even several decades.”

Hansen says we will see a massive default wave in office real estate that “will easily exceed the global financial crisis (of 2008) and could potentially even rival the savings and loan crisis.”

I believe every downtown area in America (with exception of possibly Manhattan) is now collapsing under the weight of higher prices, fewer taxes, more crime, empty office buildings, higher interest rates, and small business closures.

There’s trillions of dollars tied up in all of these places (much of it owned by Shadow Banks like Blackstone, BlackRock, Apollo, etc). And it’s all collapsing before our eyes.

So please — break free from the Denial and Procrastination phase now.

Remember Charlie Munger’s words: Denial will cause many people to go broke. Don’t be one of them.

It’s going to be bad… really bad… for millions of people over the next few years…. But it doesn’t have to be bad for you.

What can you possibly do?

My team and I strongly recommend a few critical steps…

Step #1: Avoid the Carnage

During the last great inflationary period (late 1960s to early 1980s), stocks and bonds ratcheted up and down in a brutal “sideways” motion for more than a decade.

It all finally ended with a brutal recession and the Savings & Loan Crisis, in which half the nation’s banks went under.

Most Americans are still in denial about our current situation. I hope I’ve been able to help you move past that phase today.

Because we are at such a critical moment, in addition to my own research team, I’ve also enlisted the help of my forensic accounting friend, Joel Litman, and his army of roughly 100 analysts, accountants, CPAs and CFAs.

Joel Litman works regularly with the most important institutions in America, like the U.S. Marines War College, the FBI, and the Department of Defense.

These groups go to Joel because they want the unvarnished truth about companies’ finances.

And this is why I asked Joel and his team to help us produce one of the most comprehensive Research Reports in America, detailing all the investments and assets you should avoid right now.

Our brand-new report is called: Avoid the Carnage.

It contains everything you need to know about the most dangerous financial institutions and businesses in America today. We’ll show you the companies we believe WILL NOT be able to refinance their debts.

We’ll show you the companies sitting on the biggest unrealized losses. And the industries and sectors you want to avoid at all costs over the next two years.

I can almost guarantee you have money in some of these incredibly dangerous institutions right now—and I strongly encourage you to move it.

We make it easy to get started and to figure out.

Again, everything you need to know is in our brand-new, comprehensive Special Report, called: Avoid the Carnage.

And that brings me to Critical Step #2…

Step #2: Be The Central Bank For 3,700% Gains?

As I’ve said throughout this presentation, I believe we are looking at a period that’s very similar to the late 1960s to 1980s… when inflation and interest rates soared much higher, for much longer, than almost everyone expected.

One of the things you can do in this environment is to do exactly what the world’s Central Banks did back then… and what they are doing again right now.

While this received little attention in the mainstream press, Central Banks have been buying more gold than at any time since 1967, according to the World Gold Council.

Just like in 1967, we suspect the Central Banks know something serious is brewing, and they are preparing.

The last time Central bankers made a similar move, gold soared 2,300%. (Silver did even better — up 3,700%.)

We believe it’s only a matter of time before we see much higher gold and silver prices.

In our new report, called The Power of the Central Bank, you’ll learn the best ways to buy gold and silver right now — the choices are critically important, which most people don’t realize.

For example, some gold ETFs are allowed to cash you out whenever they want, limiting your gains — while others are required to actually deliver physical gold, if you choose. It’s important to know the differences.

This report details everything you need to know about building or expanding your precious metals holdings — some of the best deals, the best mining stocks, the best gold dealers, best storage options, the best deals on physical gold, and so much more.

So much has changed in the precious metals universe over the last few years — even if you already own gold and silver, I strongly encourage you get this report in your hands now.

And that brings me to…

Step #3: America's Compounding Machines

As Nassim Taleb, an expert on financial fragility of our current system, and a man who’s probably worth more than $100 million, says,

“We are in a New Era.”

So you’ve got to be very careful about where you put your money in the stock market.

For example, there’s one small group of businesses that did NOT fall in 2022 (it’s not gold or energy, or anything like most people expect), which are still soaring higher today.

And I strongly recommend you put a significant stake of your portfolio into these companies starting immediately. I expect safe, compounded wealth over the next five years and beyond.

Just to give you one example…

There’s one U.S. firm in this group (we call it “America’s Compounding Machine”) that’s been crushing the stock market averages over the short and long term… for more than 50 years.

And get this: While the best-known and supposedly “safest” companies in America, like Google, Apple, and Amazon have fallen 11% on average since the end of 2021, the company we call “America’s Compounding Machine” went UP 32% over the same period.

Over the past decade it’s up 200% more than the overall stock market!

Oh… and I almost forgot to mention: “America’s Compounding Machine” also pays huge dividends, which goes up about 10% EVERY YEAR on average.

What’s fascinating is that there are other companies in the exact same space that have provided even bigger returns in recent years. These are businesses you can buy today and compound your wealth in the years to come with less risk.

Everything you need to know is in our brand-new Research Report called: America’s Compounding Machines.

OK, so, how much does access to our research cost, and how can you get your hands on it right away?

Here’s the deal…

Why Does No One Else in the

Financial Research Space Do This?

The three special Research Reports I just mentioned…

Avoid the Carnage, The Power of the Central Bank, and America’s Compounding Machines, will be among the first things I send you when you start a no-risk trial subscription to my research service called: The Ferris Report.

This is my team’s monthly investment report, which I deliver on the fourth Wednesday of each month.

In every report, I’ll update you on everything you need to know about the current crisis — the investments to avoid, opportunities to grow your wealth with less risk, and more.

For example, I’ve got more than a dozen recommendations in my portfolio right now. I’ve found one sector, for example, that’s performing brilliantly — because of extreme shortages, which aren’t going away anytime soon. All three of our recommendations in this space are doing great, while so many things are falling.

Of course, I’ll also keep you up to date on everything you need to know about America’s Shadow Banks, and how the next phase of this crisis is likely to unfold.

One of the things I’ve become very good at over my 22 years at Stansberry Research is helping folks avoid the biggest crashes.

In addition to warning folks about the 2007 crisis, I recently warned folks that the Nasdaq had reached a peak in 2021 on the exact day it topped out…

And I accurately warned in 2015 when the market notched its first negative return since the financial crisis.

In December 2017, I warned that Bitcoin could quickly fall as much as 90%. It plummeted by 80% over the next year.

The next year, I helped folks avoid another disaster – warning that Facebook could fall by 50% in a matter of months right before it fell 43% from July to December.

Now it might sound like I spend most of my time predicting calamities, but I reference my past calls simply because I want you to take the warning I’m sharing with you today very seriously.

And while I warned my subscribers to get out of Bitcoin in 2017 before it crashed over 90%… I also turned around in February of 2020 and told them it was time to buy… before it soared 369% in just 12 months.

Over the long run, my team and I have an unmatched track record for finding triple-digit gains with less risk…

- 150% gain on AB inBev (BUD)

- 201% gain on Alexander and Baldwin (ALEX)

- 174% gain on Altria Group (MO)

- 190% gain on Apple (AAPL)

- 125% gain on Berkshire Hathaway (BRK-A)

- 187% gain on Bitcoin (BTC)

- 111% gain on Blair (BL)

- 128% gain on Brookfield Asset Management (BAM)

- 100% gain on Circuit City (CC)

- 629% gain on Constellation Brands (STZ)

- 138% gain on Encana (ECA)

- 124% gain on Gateway (GTW)

- 142% gain on Icahn Enterprises (IEP)

- 133% gain on Intel (INTC)

- 248% gain on International Royalty Corporation (ROY)

- 100% gain on JAKKs Pacific (JAKK)

- 157% gain on Johnson & Johnson (JNJ)

- 133% gain on Latin American Export Bank (BLX)

- 113% gain on Philip Morris Intl (PM)

- 104% gain on Portfolio Recovery Associates (PRAA)

- 100% gain on POSCO ADR (PKX)

- 406% gain on Prestige Consumer Healthcare Inc (PBH)

- 212% gain on Realty Income Corporation (O)

These are obviously some of my best picks. And remember: All investments carry risk. Our past performance is no guarantee for future success. So no matter what you do, never invest more than you can afford to lose.

Over the years, my research has attracted the attention of some of the most successful people in the industry, including one billion-dollar fund manager who did seven times better than the S&P 500 between 2000 and 2018.

And like I said, we’re one of the very few firms in our industry that publishes an audited track record of ALL our recommendations, every sing year.

Of course, I can't promise you'll make big gains following our research. All investments involve risk, and past performance does not indicate future returns. Folks who don't understand that should not be reading my research, period.

But what I can tell you is this:

- We’ve had incredible success over the past 24 years helping people radically change their financial lives, by avoiding the big disasters and finding many opportunities to safely grow your wealth.

- Our work is ridiculously inexpensive compared to its value — and compared to what you’d pay anyone to manage your money for you.

- And best of all: You can try our work completely risk free. We simply don’t want your money if you’re not happy.

As I mentioned earlier…

I’ve partnered up with my friend Joel Litman and his team — so I’m going to send you their research, in addition to mine, as part of this deal too.

Joel is a Certified Public Accountant (CPA) and a forensic accountant too, who consults regularly for the Department of Defense, the FBI, and the U.S. Marines War College.

Their work I’ll send you is called Hidden Alpha. It’s an in-depth monthly stock investment research service that has a sustained track record of fantastic returns. If you were fully invested in the Hidden Alphaportfolio since our first issue, your portfolio would have returned 42%.

These guys are really good… and I want you to have their work too, in addition to mine.

So as part of this deal, you’ll receive full access to my work The Ferris Letter over the next year… full access to Joel Litman’s Hidden Alpharesearch… plus all of the Special Reports we’ve just finished putting together

So you’ll receive full access to The Ferris Report over the next year… full access to Joel Litman’s Hidden Alpha research… plus all of the Special Reports I’ve told you about.

How do you get started… and how much does it all cost?

Before I give you the specifics, there’s one more critical resource I want to send you immediately…

The Big Secret to Making

Money in a Bear Market…

As I’ve said repeatedly, I believe we’re still in the first or second inning of this crisis, and it will be much worse, and last much longer, than most people think.

And I’m not the only one saying this…

Jeremy Grantham made his name predicting the dot-com crash and the 2008 financial. He’s now warning that stocks could plunge 50% from here, and says:

“We’re by no means finished with the stress to the financial system… The low point might not arrive until “deep into next year.”

Billionaire Stanley Druckenmiller has famously never had a down year. He says the collapse of Silicon Valley Bank was just “the tip of the iceberg,” and that: “It’s just naive not to be open-minded to something really, really bad happening.”

But remember, it doesn’t have to be a disaster for you.

In fact, I’ve found a conservative way to potentially make as much as 800% over the long term, in the years to come… no matter how bad the current situation gets.

One of the world’s leading universities led an intensive study about the last time we saw similar conditions, and they found that one group of companies, which on the surface have little in common… provided great returns over the long term of around 800%, while the overall stock market fell more than 60%.

I can’t say much more about this idea here, because I think this will be THE BIG SECRET to making great gains in the coming years, while so many are losing.

I’ve written hundreds of pages about this secret already, and I want paid subscribers to get in before I say more publicly.

Everything you need to know is in my report called: 800% Long-Term Gains—Even in a Terrible Bear Market.

This report not only shows you all the data and research… but how to take advantage of it with two simple investments. You can both investment through any regular brokerage.

Again, my goal today is simple: I want to break you free from the Denial and Procrastination phase of this crisis, and spur you into action.

Please don’t fall for the idea that the bear market is over and new bull market has begun.

Remember what Charlie Munger says: Denial is how many people go broke.

No new technology, including AI, is going to save you. Make sure you are positioned to stay clear of the biggest disasters… and profit from opportunities with less risk.

To sum it all up, when you start a no-risk, trial subscription to our research today you’ll receive:

- Special Report #1: Avoid the Carnage

- Special Report #2: The Power of the Central Bank

- Special Report #3: America’s Compounding Machines

- Special Report #4: 800% Long-Term Gains—Even in a Terrible Bear Market

Plus, you’ll get the next FULL YEAR (12 issues, one delivered each month) of The Ferris Report AND the next full year of Joel Litman’s Hidden Alpha (12 issues too).

I’ll send you all the research above, in a matter of minutes.

And each month going forward, you’ll receive my latest report, and Joel Litman’s too.

This way, you’ll always know exactly what to buy and sell.

How much does it all cost?

Well, normally my work and Joel Litman’s work both cost $199 per year (about $400 total). That’s what most folks pay, and it’s a great deal for what you receive.

But today, you’ll save 75% OFF the regular subscription rates… you’ll pay just $49 TOTAL for the next full year to receive EVERYTHING I’ve described here.

And it’s all completely risk-free.

What I mean by that is, you can TRY our research for yourself and see if it’s right for you.

If not, no problem. Just cancel your subscription online or over the phone in the next 30 days, and you’ll get a full refund.

To get instant access to everything I’ve described here, click the “Get Started” button below.

This will take you to our secure online order form, where you can review everything you’ll receive once more, before submitting your order.

Thank you for your time. I hope you’ve learned something from my research today, and I hope you take advantage of this opportunity.

We are in a very dangerous time, as many people are about to find out the hard way. A few simple steps today could mean a world of difference over the next few years.

Again, to get started with our research, click the “Get Started” button below, which will take you to our secure order form.

After you place your order, you’ll have access to everything I’ve described in a matter of minutes.

Sincerely,

Dan Ferris

The Ferris Report, Stansberry Research

August 2023

Legal Notices: Here is our Disclosures and Details page. DISCLOSURES ABOUT OUR BUSINESS contains critical information that will help you use our work appropriately and give you a far better understanding of how our business works – both the benefits it might offer you and the inevitable limitations of our products. Although this is not a part of our “Disclosures and Details” page, you can view our company's privacy policy here.

© 2023 Stansberry Research

Privacy Policy | Legal Notices | Terms of Use | DMCA Policy | Do Not Sell My Personal Information | Ad Choice | Cookie Preferences